Real Estate’s preferred method of equity funding

Private Equity Waterfall is the colloquial term for the way partners distribute the share of the profit in an investment. It is common in all types of Private Equity investments and is especially prevalent in the Real Estate Private Equity industry.

The goal of a private equity investment structure is to align the interests of the various parties who invest in an individual deal or a private equity fund. Private equity waterfalls can take different forms based on each party’s goals as well as ensuring the other stakeholder has the correct incentives in the investment along with the other party.

While proper alignment requires both legal and financial mechanisms, we will focus on the distribution waterfall, which is the primary financial incentive used to align interests between parties.

These economic incentives are codified in legal documents and should be understood by all parties. A balance of sensible negative (such as clawback provisions) and positive (such as promoting interests) boundaries should be established. Investment outcomes are never guaranteed, but distribution waterfalls should provide a specific understanding of how cash flows will be shared and allow partners to ensure interests are aligned on both sides.

The term “waterfall” is used to describe how the cash from an investment flows down to the different parties involved. The top-down nature of the cash flow distributions indicates the relative priority of the parties at different levels.

Parties Involved in Private Equity Real Estate Deals

Real estate private equity deals typically involve two types of stakeholders who participate on the equity side: sponsors and investors.

Sponsors are the people who find the deals, manage the assets of the deal or the fund, and assemble the investors. They are the ones who control the deal and make day-to-day decisions about how the property or fund operates. The Sponsor is often called the General Partner (GP) and may be a single person or a firm. GPs usually contribute a small portion of the equity, but do the majority of the work involved in operating a deal or fund.

Investors are the people who contribute the majority of the equity on a deal, but do little or no work involved in operating a deal or fund. They can be individuals, family offices, pension funds, or other institutional investors. Investors are often called Limited Partners (LPs) because their liability is limited to their investment, but they also have a limited amount of involvement in the operations.

Preferred Return

The main feature of the Private Equity Waterfall which ensures the Limited Partner’s priority is the initial return paid on their capital invested as well as the return of capital. This is referred to as the Preferred Return (often simply called “pref”) because it is the first cash flow paid to equity partners.

As the primary equity capital source, the Limited Partners rightfully expect to get their initial investment back along with a nominal amount of interest. This ensures the Limited Partner receives adequate compensation for the risk taken as the majority equity capital provider in the project.

Preferred Return can be calculated using simple interest, compound interest, equity multiple, or Internal Rate of Return (IRR). The interest rate used to calculate the preferred return as well as the calculation methodology can have substantial impacts to further investment tiers. Because of the variety of options, care should be taken on the front-end to use a reliable waterfall modeling tool that is flexible and easy to use.

Understanding and modeling the different implications of these options is often the most difficult and time consuming aspect of waterfall structuring and negotiation. Discussions with potential investors often involve a lot of back-and-forth, so being able to share different variations is helpful to ensure all stakeholders properly understand the structure.

One way to experiment with different waterfall structures and collaborate with stakeholders is to use a free online Private Equity Waterfall Modeling Tool.

Investment Tiers

Some arrangements allow for the General Partner to get additional cash flow distributions if they hit certain interest thresholds. For example, in an Operating Cash Flow Promote, the GP may receive a percentage of operating cash flows, but only after the preferred return is paid. This type of structure will be detailed in the agreement and will be explicitly defined to apply to Operating Cash Flow instead of Capital Cash Flows.

After the initial tier (the Preferred Return) is hit, the investment tiers each have minimum returns that must be met before moving to the following tier.

Example Private Equity Waterfall

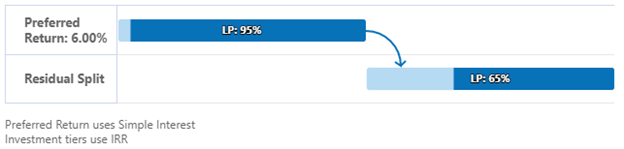

Below is a private equity waterfall diagram showing a Preferred Return with two hurdle rates that the investment must reach before the cash flow splits begin to change. The light blue bar (the GP’s portion of distributions) becomes larger (or is “promoted”) as these performance hurdles are achieved. The promotion of the GP’s interest (also called “carried interest”) is one of the keys to aligning economic interests.

Hurdle Rates at each investment tier are market driven and highly negotiated. Not only the rates, but the calculation methods (ie – simple, compounding, IRR) are dependent upon several qualitative and quantitative factors relating to the deal specifically and the GP in general.

Higher risk deals that have more intermittent cash flow and longer payoff periods or uncertain outcomes will draw fewer investors and allow LPs to command better terms. Safer bets put the power in the hands of the GPs to get larger distributions earlier. The same logic applies to the historical performance of the GP.

Those with strong track records and long lists of previous investors pay the lowest preferred return rates and are promoted faster than counterparts with less experience. LPs also tend to hedge risks with greener GPs by including a clawback or limiting incentive fees.

Residual Split

Once all hurdles have been achieved, any remaining cash available will be split between the Limited Partner and General Partner based on one last percentage share. This final tier is referred to as the residual split.

In simple waterfalls, this may be the only “promote” a General Partner can earn. This is common with family offices or High Net Worth Individuals (HNWIs) who aren’t looking for complicated investment structures. In more sophisticated structures, this is the final bucket in a multi-tiered waterfall.

These are designed for the GP to achieve specific milestones and need to be rewarding enough to encourage the GP to work hard for the investment to perform well. Institutional investment groups often prefer this method to reduce risk when working with a wide array of GPs on different investments.

Private Investors

Existing relationships between LP and GP can certainly play a role in the private equity waterfall structure. Stronger ties allow for simpler arrangements with a straightforward structure. On the other hand, investors that haven’t previously worked with a GP may request their full principal investment to be paid back entirely before the GP earns any additional cash flow. This not only motivates the GP to hit performance targets quickly, but also ensures the investor is able to get their invested capital returned as soon as possible.

As mentioned above, in some cases the GP will “earn a promote” on the cash flow distributions before the initial equity investment is paid back. This often happens when the LP desires consistent cash flow and they want to provide an incentive to the GP to ensure this happens. This can also happen with experienced GPs that have worked with the same investors before and the LPs are willing to share in the performance from the outset.

Allowing the GP to “earn a promote” will theoretically help motivate them to focus on the success of the investment to continue to outperform throughout the hold period. Since LPs are passive and primarily financially motivated while the GP retains control, this structure further aligns their interests. The way these tiers and calculations are structured can vary based on the type of investor and what value the investor is bringing to the investment.

High Net Worth Individuals (HNWIs) are common investors in private equity real estate deals and they typically look for more straightforward equity waterfall investment structures. This can lead to a simple split of cash flows between the GP and LP once the preferred return has been satisfied. The below example can be referred to as a single promote structure, because there is only one opportunity for the GP to earn an additional share in the investment.

Institutional Real Estate Investors

Institutional Real Estate Investors tend to scrutinize deals more heavily because they represent a collection of investors. They act as more of a fiduciary and will likely have significant real estate experience and a sophisticated understanding of investments. Investors in an institutional fund are able to diversify with smaller individual investments spread across more deals.

For all these reasons, institutions take a more conservative approach when vetting general partners and negotiating waterfall structures while leveraging their underwriting expertise and financial strength. Waterfalls with Institutional Real Estate Investors commonly have multiple tiers (preferred return and one or more hurdles) and involve complex calculations to accurately match the requirements of their overall investment portfolio.

Private Equity Waterfall Example

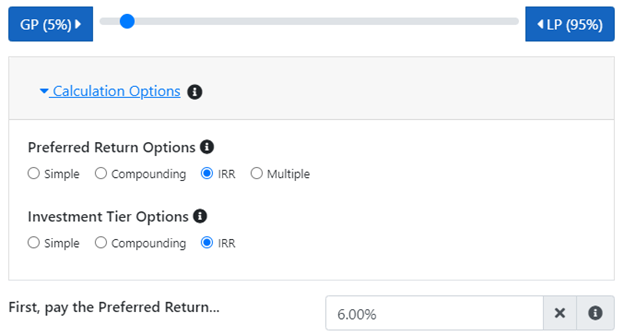

Below is an illustration of a two-tiered waterfall with a 6% preferred return, an 8% hurdle, and a 50/50 residual split to the investor and general partner. Assume a GP contributes 5% of the equity required for a real estate investment and raises the remaining 95% of the equity with a 6.00% preferred return, both using an IRR calculation.

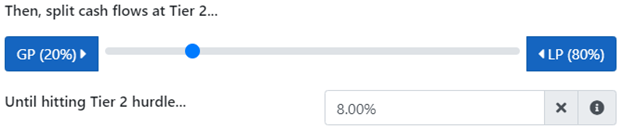

After the preferred return, the first tier splits the cash flows so the GP receives 20% and the LP receives 80%, but only until the LP receives an 8.00% IRR.

After reaching 8.00%, any remaining cash will flow into the residual split (not to be confused with residual value or exit events). Residual refers to any cash left over after hitting all lower investment tiers. It is essentially a final tier without a hurdle cap. The term “residual” is usually not part of the agreement but is used commonly.

For our private equity waterfall example, it will be a 50/50 split, with the GP and LP receiving equal portions of the excess cash flow.

After setting up this structure, the following diagram shows all these pieces together…