PLEASE NOTE THAT THIS TOPIC IS MOVING QUICKLY AND COVID-19 REAL ESTATE IMPACTS MAY CHANGE FREQUENTLY. ENSURE YOU CONSIDER THE DATES EACH REPORT WAS PUBLISHED.

We all got it wrong.

Every year, we compile and summarize available real estate research reports to inform our clients about the broad spectrum of potential risks and opportunities in the coming year. By the time we were done putting together our annual Real Estate Research Roundup — Outlook this year, COVID-19 had already taken hold, likely making virtually every one of these reports irrelevant.

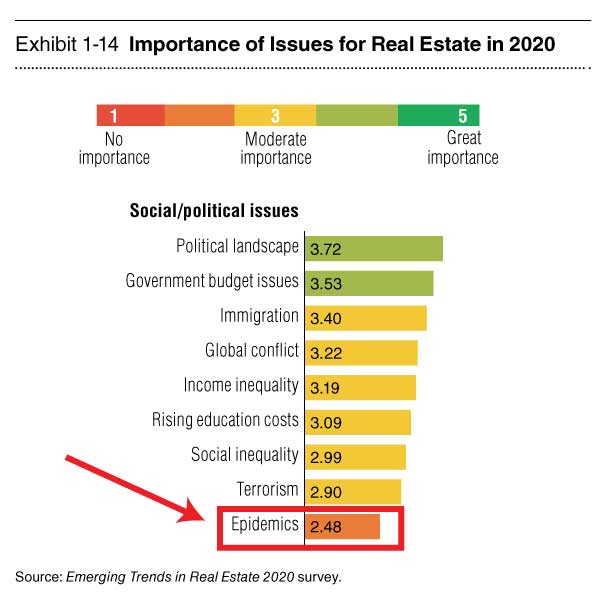

One of the most comprehensive reports is the PwC / ULI Emerging Trends report, which surveys more than 1,500 industry participants and conducts over 750 in-person interviews of top executives.

The above chart, which is a snippet from that report, shows that out of all these highly influential and informed leaders in our industry, the topic of Epidemics was last on the list. It literally just wasn’t on anyone’s radar at all.

As the bears take over on Wall Street, there are plenty of experts weighing in on the impact COVID-19 will have on the global and U.S. economies, financial markets and commercial real estate. It is likely too soon to tell how far reaching the effects will be, or exactly how long they will last. That uncertainty inevitably makes capital more cautious in its decision making and due diligence. At the same time, commercial real estate investors and developers are continuing to reevaluate strategies as it relates to immediate, short-term and longer-term opportunities.

CREModels maintains a comprehensive list of commercial and multifamily real estate research for investment and development. We have added the latest industry analysis on COVID-19 real estate impacts to help you better understand this dynamic, rapidly changing situation and navigate in the current climate. We have provided short overviews of the more comprehensive reports and links to all of them, so you have a single source for the latest information. We will attempt to update this page regularly, so please check back often and subscribe to our email list to remain informed.

We have compiled and summarized several of the available reports on the topic to help keep you informed as best we can.

Please take a look and make sure you are managing your business prudently and staying safe.

If there’s any way we can help, let us know

It is important to note that the information below is our attempt to distill research reports which include the opinions of others, and none of the information included should be deemed advice or forecasts provided by CREModels.

Major Real Estate Resource Centers

Upcoming webinars covering the topic…

We will attempt to keep this list up-to-date with upcoming webinars on the topic. After they have taken place, we will move them to the section below with links to the recordings when available.

Prior Webinar Replays

These are the links to webinars that have already taken place, but are now available as recorded sessions.

FS Investments – Macro matters: COVID-19 widens reach into U.S., causing market volatility to surge

FS Investments has been posting frequent updates on the coronavirus and COVID-19 real estate impacts. The latest analysis from Lara Rhame, the firm’s chief U.S. economist and managing director, posted another update on March 11th. The analysis takes a closer look at U.S. economic risks and resiliency, as well as the potential for further policy response.

- Volatility is the new normal: Equity markets suffered the worst price decline in over a decade on Monday, March 9, as the Dow fell more than 2,000 points and the S&P 500 ended the day down -7.60%. The sell-off became so severe that market circuit-breakers were automatically triggered for the first time since 1997.

- How low will rates go? The Fed’s surprise 50 bps rate cut to 1.00–1.25% contributed to a further slide of interest rates across the U.S. Treasury curve. The 10-year Treasury hit a new record low on March 9th, at one point falling as low as 0.33%. The MOVE Index, which measures forward-looking Treasury market volatility, spiked to 163.7 on March 10th, which was the highest level since 2009.

- Economic impact: On the positive side, the U.S. economy is the biggest in the world, and arguably the healthiest and most resilient. The February payroll report showed that the economy added 273,000 jobs and the unemployment rate fell back to 3.5%, a multi-decade low.

- New policy moves: In addition to the early March rate cut by the Fed, markets are expecting over 50 bps of rate cuts at its March 18 meeting, and some expect the Fed funds rate to be back to zero by June. In addition, discussion of fiscal stimulus, including payroll tax cuts, is ongoing.

Cushman & Wakefield reports on impact of COVID-19 on real estate markets

It is a fluid situation, and there is tremendous uncertainty regarding how broadly the virus will spread and what its ultimate impact will be on health policy, economic growth and financial and real estate markets. Cushman & Wakefield’s early observations and initial assessment of how the outbreak may impact the property markets going forward include:

- Central banks are responding aggressively. In addition to the Fed rate cut, the People’s Bank of China has deployed several new stimulus measures, and central banks in Indonesia and Singapore have also stepped up support.

- It is important to note that the commercial real estate sector is not the stock market. It’s slower moving, and the leasing fundamentals don’t swing wildly from day to day. Certainly, if the virus has a sustained and material impact on the broader economy, it will have feedthrough impacts on property as well. However, it’s still too early to gauge any fallout.

- The outbreak has prompted a flight to quality, driving investors into the bond markets.

- If past outbreaks are a useful guide, then COVID-19 should largely be contained by the first half of 2020. Most anticipate a strong rebound in markets in the second half of the year.

- The global economy was gathering momentum heading into 2020. Assuming infections globally will abate by mid-year, and with more government stimulus now going in, market conditions could be primed for a rebound as pent up demand is unleashed.

Marcus & Millichap Special Report on Coronavirus and the Implications for CRE

Marcus & Millichap is supporting the view that the economy is sturdy enough to withstand current headwinds from COVID-19 and a recession is not imminent. That being said, the virus will weigh on the U.S. economy in the first quarter due to weaker exports, reduced tourism and supply chain-related shortfalls. On the positive side, the U.S. economy still has low unemployment and relatively strong consumption levels that should help the economy weather the short-term effects of the virus.

Report highlights include:

- Concerns about the spread of the coronavirus is causing a flight to safety that has driven interest rates to a record low.

- Historically, pandemic outbreaks such as SARS, the H1N1 “swine flu,” and the “avian flu” or “bird flu” generated short-term market instability that moved toward stabilization over the following three to six months.

- The volatility of equity markets reiterates the stability of commercial real estate and the compelling 5-7% yields.

Moody’s Offers Free Coronavirus Credit and Economic Research

Moody’s Corporation announced in early March that it will be offering its research and views on the credit and economic impact of the coronavirus via a dedicated website available to the public at moodys.com/coronavirus. The site brings together insights from across the company to help market participants to better understand the financial implications of the outbreak. In addition, the site will be updated on an ongoing basis.

Moody’s has published over 100 reports and other content on the impact of COVID-19 on issuers and market sectors and geographies, including analysis from both Moody’s Investors Service and Moody’s Analytics. Some examples of the research included on the website include:

JLL analysis tackles fact vs fear on coronavirus

The coronavirus presents the first global crisis since the Great Recession. There are still many unknown variables that will dictate the impact on the global and U.S. economies. In the U.S., the impact will depend largely on the response function from consumers, businesses, and government. The analysis published March 4th. Based on information available at that time, JLL Chief Economist Ryan Severino was predicting a best-case scenario with relatively limited impacts from coronavirus that has now reduced the baseline GDP forecast for the U.S. to roughly 1.5%, down 30 basis points. However, the probability of a downside scenario occurring has increased notably in the past week.

Downside scenario: If response to the virus causes consumers to cut back on typical activities, avoid going to work, quarantining inside their homes, etc., that could produce a significant exogenous aggregate demand shock – a sudden, but temporary decrease in the demand for goods and services. In particular, consumption has risen to 70% of the U.S. economy. Private investment also could weaken further as businesses sour on deploying capital in an uncertain health environment.

Typically, an aggregate demand shock temporarily lowers GDP and reduces prices. If workers stay home (voluntarily or involuntarily) and cannot telecommute because their jobs cannot be done remotely, that could also produce an aggregate supply shock to goods and services. The simultaneous combination of a demand shock and supply shock could cause a more severe and potentially prolonged downturn. The duration of the response matters too. All other things equal, the shorter the duration, the better for the economy.

Avison Young briefing on COVID-19 and the impacts on CRE

Avison Young’s base case assessment of the impact on the real estate market assumes that there will be further spread of the virus across and within countries, but that the outbreak will be contained before it causes extreme economic disruption. Some key points noted in the economic summary include:

- Disruptions in business activity will have a ripple effect that will slow economic growth in the short-term, but a degree of bounce back is likely, albeit unevenly distributed.

- Commercial real estate will see secondary impacts from reduced economic activity and temporary “wait-and-see” disruptions as elevated uncertainty and risk will cause some businesses to delay investment or expansion plans.

- Demand for real estate investments remains high, with multiple sources of capital active in the market. The scope of any market impacts will depend on how the disease evolves, but cross-border investment in particular is likely to slow in the short term.

- Longer term, the changes that businesses and individuals will implement during the crisis will accelerate some trends already evident in the market, including de-globalization of supply chains and a shift towards online retail and flexible working practices in the service sector.