Commercial Real Estate Price Volatility & Opportunity

Author:

Managing Director

LOS ANGELES – Commercial Real Estate prices may fall up to 5% over the next 12 months, according to a report released by PIMCO. Yet certain investment strategies and platforms may find extraordinary opportunities as a result.

Price Gains Coming Largely from Capital Flows

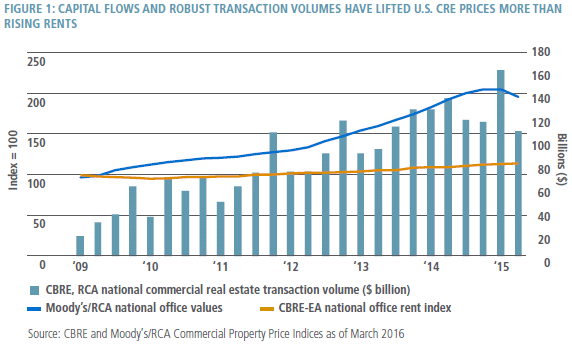

According to the authors, John Murray and Anthony Clarke, the disconnect between commercial real estate prices and the rents charged for occupancy in those same properties is a concerning data point.

Since the fourth quarter of 2009, overall office prices have doubled (as have general CRE prices), yet national office rents have risen only about 15%.

A PIMCO report suggests that capital flows, not fundamentals, deserve credit for the recent rise in commercial real estate prices

PIMCO believes this disconnect signals that the drastic increase US commercial real estate prices has come from capital flows. While this has been a boon to pricing, questions remain how buoyant a force this will be going forward.

Indicators of unstable sources of capital flows include:

- Daily returns of Real Estate Investment Trusts (REITs) have been highly correlated to the S&P 500 while trading at a discount to their Net Asset Value (NAV) of their underlying real estate holdings over the past 18 months

- REIT acquisitions accounted for approximately 15% of total transaction volume from 2012 through 2014, yet by the second half of 2015 this contribution had dropped to only 8%

- The difference between NAV and REIT valuations has forced many REITs to become net sellers of assets

Regulations on Broader Financial Sector Causing Domino Effect

Regulations enacted after the recent financial crisis such as Dodd-Frank and the Federal Reserve’s Comprehensive Capital Analysis and Review (CCAR) have intensified these effects, with little or no connection to the commercial real estate market. Because the real estate industry relies heavily on debt to fuel transaction velocity, this creates a domino effect in the market.

Examples of the regulatory domino effect:

- Volatility in the broader high-yield debt market led to redemptions that forced hedge funds to sell-off subordinate Commercial Mortgage Backed Securities (CMBS), of which they own approximately 40% of the positions

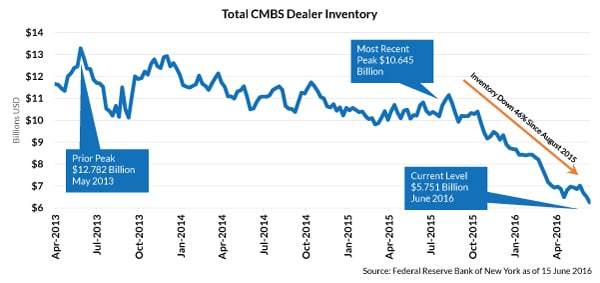

- This type of sell-off would normally be back-filled by banks, but under regulatory pressure, they have reduced their balance sheet inventory by almost half in the past two years

- Without the bank backstop, prices for these positions have tumbled more than 20%

- A consequence of this drop in prices is that CMBS originators ended up with underwater loans that are no longer able to be securitized

- CMBS issuance in the first quarter of 2016 dropped by over 30%

- CMBS accounted for over 20% of the real estate debt market in 2015, and this has dropped to only 11% in the first quarter of 2016

Total CMBS Dealer Inventory has fallen 46% between August 2015 and June 2016

Regulatory Pressures Still to Come

All these issues are what we’ve already seen happening in the market: it’s hindsight. Looking ahead, there are still regulatory pressures yet to come. New risk-retention rules will hit CMBS originators later this year, requiring they retain at least 5% of any new securitizations. (Related: Preserving Access to CRE Capital Act)

In essence, bank originators will have to go from a “moving business” model to a costlier “storage business” model.

Non-traded REITs have also found themselves in the regulatory cross-hairs. New rules require non-traded REITs to disclose valuations based on the underlying value of the real estate in their portfolios. This has been a one-two punch for several, not only affecting the reported NAV but also reducing fundraising by 30% in the year-ending January 2016. Now is an opportune time for investors in both public and private REITs to independently evaluate NAV of the assets supporting their equity investments.

Flight to Quality Will Affect Secondary and Tertiary Markets Disproportionately

All the issues discussed above indicate problems affecting the overall commercial real estate market, but by its very nature, the market is highly fragmented and location-specific. Smaller investors such as non-traded REITs hold higher concentrations of assets in secondary and tertiary markets because they lack the level of access to capital enjoyed by their publicly-traded brethren. Clearly these markets will feel the effect of buyers who have less capital to spend and are subject to increased impairments. Commercial real estate principals and investors with holdings in these markets should consider stress-testing portfolios and assets to ensure compliance with debt covenants and understand effects on equity distributions and returns.

Maturities are No Longer the Elephant in the Room… the Time is Here

We have been hearing about the “wall of maturity” for years now, as the $200 billion in 10-year term CMBS loans originated in the peak years of 2006-2008 begin to come due. Also, there are another $50 billion in 10-year term non-CMBS commercial real estate loans and equity funds which will reach maturity during this period. Many lenders and private equity real estate fund managers have retained these assets in an effort to generate fees and/or earn lucrative promotes at disposition.

Foreign Capital May Buoy Prices & Come to the Rescue

Sovereign wealth funds throughout the world, which are currently under-allocated to commercial real estate, have historically viewed the US market as a safe haven. In recent years, they have increased their commitments to commercial real estate and in 2015 these efforts accounted for over 10% of the transaction volume in the United States. Clearly risks exist when such a large slice of the overall real estate debt market comes from outside the US.

While increased reliance upon foreign capital is not necessarily an envious position, any offsetting effect may be welcome as the global economy outside the United States becomes more uncertain.

Investment Opportunities Exist in Uncertainty and Volatility

Despite the report’s prediction for a 5% decline in prices over the next 12 months, opportunistic funds with dry powder are well-positioned to take advantage of price dips in secondary and tertiary markets. Debt investors with the skill to comb through complex CMBS structures and have the ability to quickly model individual tranches against their underlying asset values may be able to take advantage of pricing missteps amid an otherwise difficult environment. Investors in public markets may find REIT pricing discounted to the point that attractive share purchases can be made at levels well below the NAV, while gaining the advantage of liquidity.

Sources:

Link to the Report: US Real Estate: A Storm Is Brewing

Links to the Data in this Report:

Moody’s CPPI – Apartment Price Gains Continue to Counterbalance Commercial Price Declines

Preqin – Sovereign Wealth Fund Review

CBRE – Global Office Rent Cycle MarketView Q4 2015 (No longer available)

Bank of America – Who’s financing maturing legacy conduit loans?

Dow Jones – REIT Index

Green Street Advisors – Real Estate Securities Monthly

New York Federal Reserve – Primary Dealer Statistics

(Net Positions > Mortgage-backed Securities > Non-Agency MBS > Other CMBS)

Commercial Real Estate Industry Terms & Acronyms:

NAV – Net Asset Value

CRE – Commercial Real Estate

REIT – Real Estate Investment Trust

CMBS – Commercial Mortgage-Backed Security

Dodd-Frank – The Dodd-Frank Act: A Cheat Sheet

CCAR – Federal Reserve Comprehensive Capital Analysis and Review

Other Coverage:

Bloomberg.com – PIMCO Says ‘Storm Is Brewing’ in US Commercial Real Estate

The Real Deal – Stormy future for US commercial real estate, PIMCO says

Business Insider – PIMCO: A storm is brewing in the real-estate market

MarketWatch – A storm is brewing in the real-estate market, PIMCO warns

Investopedia – PIMCO Forecasts Drop in Commercial Real Estate

InvestmentNews – PIMCO issues urgent warning about state of commercial real estate market